Meta has revealed its newest quarterly efficiency replace, which exhibits a rise in complete customers throughout its Household of Apps (Fb, Instagram, WhatsApp, Messenger and Threads), and a bounce in income in This autumn 2026.

Which is sensible, given the vacation marketing campaign rush, but it surely underlines Meta’s dominant market place, which can be certain that it could actually wager massive on future tech, and the following stage of digital connectivity.

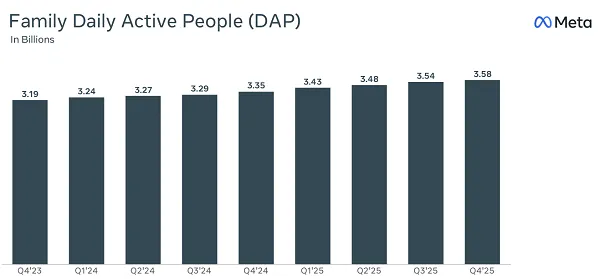

First off, when it comes to customers, Meta added 40 million customers in This autumn, taking it to 3.58 billion day by day energetic customers throughout its apps.

Which stays a really spectacular quantity, and one that you just most likely must take a step again from to essentially recognize. The inhabitants of the world is round 8 billion individuals, so the truth that 45% of them are utilizing a Meta app on daily basis, when that additionally contains individuals aged beneath 14, and the aged, is a loopy level of be aware.

What’s barely fascinating right here is that Meta additionally claims to have deleted 544,000 profiles in Australia in response to the Australian authorities’s newly applied teen social media ban, which restricts social apps to these over the age of 16.

544k might be too small a quantity to essentially make a dent in Meta’s general figures, however there’s no actual indication of any slowdown in Meta’s consumer numbers, which may counsel that teen customers are merely beginning new accounts to bypass the brand new age detection measures.

Both approach, extra continued progress for Meta’s apps, which one way or the other hold including tens of millions of customers each three months, regardless of presumably reaching saturation level in lots of areas.

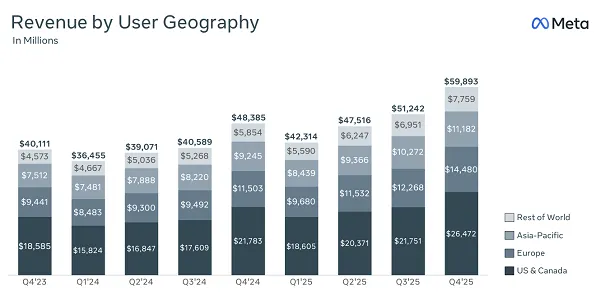

When it comes to income, Meta introduced in $59.89 billion for the quarter, taking it to $200.97 billion for the total yr.

Meta noticed an anticipated increase in advert gross sales over the vacations, which boosted its efficiency, whereas it additionally continues to see sturdy gross sales of its AI glasses, including one other income path.

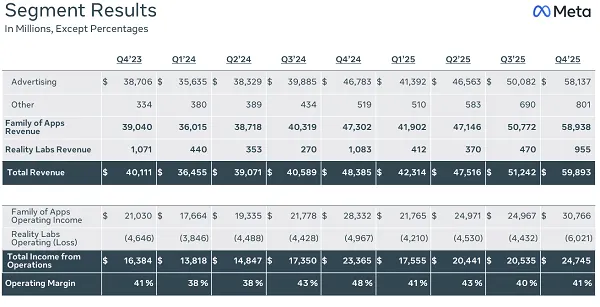

Although Actuality Labs, its VR/AR division, remains to be dropping some huge cash.

As you may see, Actuality Labs noticed a $6 billion loss within the interval, which isn’t shocking, given its ongoing funding within the tech, because it seems in direction of the longer term. However it stays a big blight on Meta’s books.

Meta’s additionally gained a brand new income stream in Threads Adverts, which at the moment are out there to all advertisers, whereas it continues to push Meta Verified subscriptions with expanded choices.

Meta Verified take-up additionally appears to be rising, with its “Different” income stream bringing in $801 million for the interval, a rise of $572 million for the reason that launch of Meta Verified in Q2 2023.

Meta doesn’t present a breakdown of the contributors inside this aspect, however that’s a big improve in “Different” income for the reason that introduction of the providing, which, at a median of $15 per subscriber, may correlate to round 30 million or so paying Fb and IG customers.

That’s not an actual breakdown, as there are different parts that contribute to this determine. However both approach, it’s one other feed in for Meta’s coffers, which contributes to its general cash pile.

Which is necessary for its massive image planning.

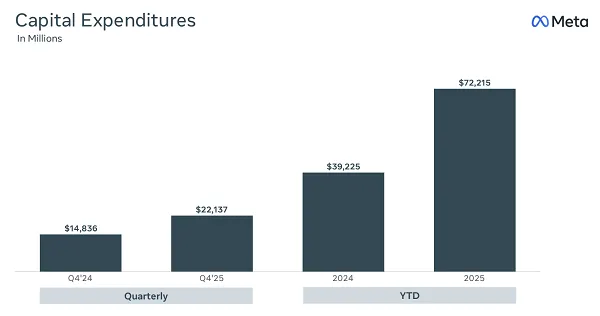

Meta stays targeted on its long-term bets, which implies short-term impacts, because it outlays tons of of billions ($70 billion final yr alone) to construct expansive new AI knowledge facilities.

To be clear, Meta has been engaged on the event of AI for over a decade, and is properly forward of OpenAI or xAI on this entrance. However OpenAI modified the sport with ChatGPT, which doesn’t use AI as such (there’s no “intelligence” or pondering in ChatGPT’s course of), however as a substitute is a re-angling of machine studying, in a approach that replicates conversational language.

So whereas it might look like you’re getting human-type responses from the most recent AI chatbots, these are actually simply knowledge matching, figuring out what probably symbols correlate with those who you’re entered as a question. The notion then is that these instruments are offering you with a thought-about reply, however ChatGPT has no idea of the output that it offers, it’s simply supplying you with essentially the most logical, data-matched output based mostly on its reference sources.

True AI extends past this, and can replicate neurons within the human mind with digital parts. That’s what Zuckerberg is working in direction of, and it looks like the arrival of ChatGPT has reiterated his want to be the pioneer on this entrance, and ship actual AGI to the world.

We’re not near that but, however that’s what Meta is constructing in direction of, which may ultimately give Meta an enormous benefit within the broader market, if it could actually truly simulate human-like thought inside a machine.

Or it’ll kill us all, however a method or one other, that’s what Meta’s “Superintelligence” staff is working in direction of, a step past the present instruments that we’re now referring to as AI.

So whereas most individuals now view AI because the generative AI instruments we’ve, which use the web as their mind (and can at all times be each fallible and restricted due to this), Meta’s actual intention is the following stage, which can have actual functions when it comes to replicating and increasing human thought.

So what does that imply for the metaverse, and Meta’s different long-term wager?

Many noticed Meta’s current job cuts in its Actuality Labs division as a sign that it’s scaling again its metaverse ambitions, however I noticed this extra as a mirrored image of Meta’s more and more reliance on AI instruments for coding and engineering work.

Throughout an look on the Joe Rogan podcast, Zuckerberg mentioned the speedy growth of AI programs, and famous that:

“In all probability in 2025, we at Meta, in addition to the opposite corporations which are mainly engaged on this, are going to have an AI that may successfully be a kind of mid-level engineer that you’ve at your organization that may write code.”

That is particularly related for VR growth, with AI programs now enabling simplified VR object and setting creation based mostly on conversational prompts.

I think that, no less than a part of Meta’s job planning entails a share of some work being outsourced to its evolving AI processes, and as famous, that may very well be notably related in VR growth.

Does that imply that Meta doesn’t suppose VR would be the subsequent airplane of digital connection?

Whereas I do suppose that there are some important challenges in VR adoption, apart from compelling choices to spice up take-up (like movement illness and the psychological impacts of VR immersion), I additionally consider that, logically, the VR metaverse does make sense as the following evolution of on-line connection.

We’ve moved from text-based messages to photographs to video, as technological advances have enabled such. VR looks like the logical subsequent step, and while you additionally take into account that the following era of shoppers are already conducting loads of their social interactions in metaverse-like areas, by means of gaming worlds, this all aligns, and factors to VR being a big future alternative.

Meta’s eager to steer the AI cost for the second, as a result of it presents such important alternatives for an keen market, however don’t take its staffing modifications as a definitive indicator of a transfer away from VR (the truth is, Actuality Labs chief Andrew Bosworth has reiterated that Meta will proceed to spend money on VR, whereas cellular adoption of Horizon Worlds is rising).

Given all of those future-looking issues, it’s onerous to take a lot away from Meta’s earnings, aside from it continues to strengthen its core enterprise, which can give it a strong basis for such funding.

Whether or not that funding pays off is one other factor, however Meta is eyeing these future areas of alternative, and might be well-placed, if not best-placed, to capitalize on such when the time comes.