Snapchat has reported its Q3 efficiency replace, which exhibits optimistic progress on a few key fronts, although some considerations nonetheless stay, significantly by way of rising prices, that are solely set to leap increased within the new 12 months.

First off, on customers. Snapchat is now as much as 477 million day by day actives, which is a rise of 8 million on Q2.

Which is just about the identical as the rise that it’s posted every of the previous couple of quarters, with all of Snap’s consumer development coming within the “Remainder of World” class. Certainly, Snap added no new customers within the U.S. or Europe, with each areas seeking to have stalled out, or reached saturation level for the app.

Which caps Snapchat’s development, and with extra areas now contemplating increased age restrictions for social media use, that’s not a fantastic signal for Snap’s ongoing alternatives.

Snapchat has addressed this concern in its accompanying notes, explaining that:

“These coverage developments, mixed with potential platform-level age verification, are more likely to have unfavourable impacts on consumer engagement metrics that we can not at present predict.”

Yeah, that’s not a great signal, and whereas Snap does additionally be aware that it’s utilizing new alerts from Apple and Google to find out consumer ages (?), that can seemingly have a huge impact on platform utilization, particularly in markets the place Snapchat’s not including any extra customers.

That’ll restrict the platform’s monetization potential. And whereas constructing in growing markets will present longer-term alternatives, its speedy consumption may take a success.

However proper now on the income entrance, issues are trying okay:

Snapchat introduced in $1.5 billion in income for the quarter, pushed, it says, by:

“Continued development in our small- and medium-sized enterprise (SMBs) prospects, and enhancements in direct response promoting efficiency”

Snapchat’s been working to enhance its advert concentrating on instruments, and placement choices, and it looks like these efforts are having a optimistic influence, with extra advertisers seeking to faucet into the app’s reputation with youthful customers to increase their attain.

Snapchat’s additionally now bringing in $750 million per 12 months from Snapchat+ subscriptions. So even with much less development in its core income markets, it’s benefiting from what it’s bought.

And it’s additionally reassessing its enterprise method to place extra give attention to its key income markets:

“This consists of testing adjustments to our infrastructure that can decrease prices in areas with much less long-term monetization potential, permitting us to raised align our sources with the monetary alternative of every geography, however probably coming at the price of hostile trade-offs with engagement in these international locations.”

As a result of once more, whereas including extra customers, as a high line quantity, appears to be like nice, the actual fact is that Snap shouldn’t be going to be incomes as a lot income from these customers, resulting from regional income variances. Snap is addressing this, nevertheless it’s an vital acknowledgement, which highlights this as a key concern, versus seemingly hoping the consumer depend will distract traders.

When it comes to utilization, Snap says that international time spent watching content material has elevated year-over-year, “reflecting our multi-year funding in machine studying and the continued power of Highlight.” Snap says that it’s launched its largest content material advice mannequin thus far, “enhancing freshness and relevance throughout the platform,” whereas it’s additionally upgraded its infrastructure to “get a step nearer to delivering content material in close to real-time, lowering latency and reducing mannequin coaching cycles from days to simply two hours.”

Highlight has grow to be a key engagement driver for the app, with views in its short-form video feed rising greater than 300% year-over-year within the U.S.

Brief-form video is probably the most partaking format on all social apps, so that is no actual shock, nevertheless it’s attention-grabbing to see Snap re-purposing TikTok’s core providing, in the identical approach that Instagram repurposed Tales.

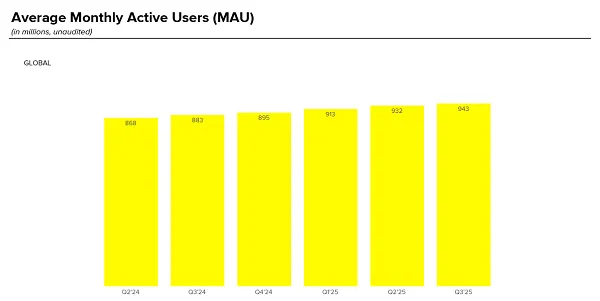

Snap has additionally reported that month-to-month energetic customers are actually as much as 943 million, closing in on that one billion consumer milestone.

So some good indicators, with Snapchat seeking to refocus its enterprise round its core alternatives, whereas it’s additionally introduced a new take care of Perplexity to combine Perplexity’s AI-powered reply engine straight into Snapchat.

Extra alternatives for extra engagement, and maximize its viewers potential. Though there’s one different aspect that’s additionally of concern.

Snapchat’s prices are nonetheless rising, and with the corporate seeking to launch its AR-enabled Specs subsequent 12 months, these prices are inevitably going to rise even additional, for a product that also appears unlikely to be the best choice available on the market.

Meta’s AI glasses already provide higher performance, and with each Meta and Apple launching their very own AR glasses within the close to future, the chance for AR Specs appears restricted.

Nonetheless, Snap’s sticking with it, although it has additionally, not less than reportedly, thought of spinning off Spectacles into its personal enterprise, in an effort to restrict the impacts on Snap.

That looks like a great method, albeit a fancy one, as a result of I proceed to imagine that AR Specs are going to grow to be an albatross for the corporate, which can tank its valuation by the top of subsequent 12 months. And it doesn’t have the strong advert enterprise of its opponents to fall again on, so it could possibly be a troublesome time forward, until Specs are an absolute hit out of the gate.

I don’t see that taking place, however the hype round its unique Spectacles was excessive when it first launched them again in 2016 (even when they did find yourself costing Snap cash resulting from unsold stock).

Perhaps, that preliminary hype will result in a extra optimistic alternative for AR Specs.

We’ll discover out in just a few months.